Gauging the growth in domestic content in the solar supply chain, Anza shares Q2 2025 domestic content insights amid uncertainty.

Anza, a subscription-based data and analytics software platform, released its Q2 2025 Domestic Content Insights report that reveals trends in domestic manufacturing of solar modules and battery energy storage systems (BESS). While only four months following Anza’s last report, dramatic shifts in U.S. domestic content and trade policy caused Anza’s Strategic Sourcing Team to communicate with manufacturers in order to update the platform with pricing and availability for solar modules and energy storage systems that includes tariffs brought by the International Emergency Economic Powers Act (IEEPA) tariffs and Section 301 duties.

Anza analysts note that the result of dramatic policy changes is pricing uncertainty for manufacturers, developers and buyers alike, which can cause buyers to delay procurement decisions or re-evaluate sourcing strategies.

The domestic production strategies continue to evolve in response to shifting market conditions and regulatory updates. Manufacturers are actively adjusting their domestic content plans. Some are accelerating U.S. production timelines to take advantage of domestic content incentives and avoid tariff exposure. Boviet Solar, for example, just opened a module facility in North Carolina with plans to add cell production next year. ES Foundry is already producing cells in its new plant in South Carolina.

Anza notes that other manufacturers have canceled previously announced plans due to financial or logistical constraints. In February, Premiere Energies, a cell manufacturer based in India, halted plans to manufacture 1 GW of cells in the U.S. amid uncertainty. In the same month Freyer Battery abandoned plans for a battery factory in Georgia. (Freyer subsequently rebranded as T1 Energy and announced it will become a vertically integrated solar and battery storage supplier based in Texas, after its acquisition of Trina Solar’s U.S. manufacturing assets.)

Solar modules and cells

According to the Solar Energy Industries Association (SEIA), since passage of the Inflation Reduction Act of 2022, there have been more than 100 new solar and storage manufacturing announcements with 84 new solar and storage manufacturing facilities coming online, with 55 facilities under active construction.

Anza says that the availability of U.S. assembled modules is projected to fluctuate over the coming years, while the number of suppliers producing both U.S.-made cells and modules is expected to increase gradually. For clarification, U.S. assembly means that the final module is assembled in the United States. All U.S. made cells are also assembled in the U.S.

The good news for the solar supply chain is that the numbers are rising for both modules and cells, although there is still more module manufacturing than cell because cell manufacturing takes a greater investment in time and financing. In the Q1 report there were 12 suppliers with U.S. assembled modules and seven cell. The Q2 report shows 17 module suppliers and five cell.

Expectations also rise with time on the module side, but not so much for cells. While the Q1 report expected 12 module suppliers in 2H 2025, the current report shows 18; however, cell suppliers drop from the seven expected in the last report to 5 now—no change from the first half. The chart below shows that it will take until 2H 2027 for cell suppliers to number in the double digits; however, the gap is expected to close at that time, with 18 module suppliers to ten cell.

Anza notes that the temporary increase to 20 suppliers in 1H 2026 shown in the chart above reflects a short-term commitment that some manufacturers are unwilling to extend further out. Likewise, the drop in 2H 2026 and 1H 2027 may be an unwillingness to commit. “Recent tariff announcements are also prompting suppliers to be more cautious about long-term projections,“ Anza said.

Key takeaway: Anza projects a 100% increase in U.S.-made solar cell production from five suppliers in 1H 2025 to ten in 1H 2027, indicating a growing commitment to integrating U.S.-made cells in module production.

Battery energy storage systems (BESS)

Anza tracks containers, modules and cells, individually, which an Anza spokesperson told pv magazine USA provides insights into the stages of domestic manufacturing adoption and their alignment with IRS guidance. For example, each component of a battery energy storage system contributes points under the 2025-08 IRS Notice, which helps projects meet the domestic content qualification thresholds.

This report finds that the BESS sector is experiencing rapid growth in domestic manufacturing. The Q1 2025 report projected that by 2H 2025 two suppliers were expected to be providing fully domestic cells, modules and containers. Now Anza forecasts three BESS cell suppliers and seven supplying each modules and containers.

As shown in the chart below, the forecasts more than triple for battery cell suppliers from 2H 2025 to 1H 2027. Domestic module production is expected to jump 267% in that same time period. Container suppliers will more than double from 1H 2025 to 1H 2027.

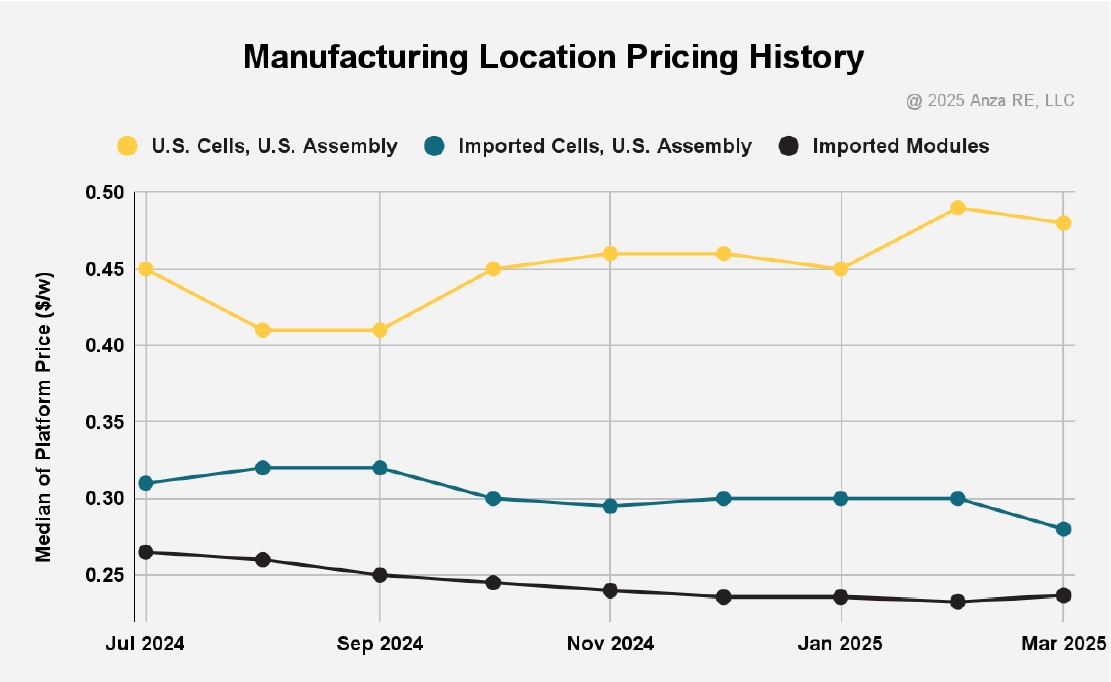

Manufacturing pricing dynamics of solar cells and modules

Like last quarter, domestic solar modules are in high demand and short supply. Suppliers are charging a premium for fully domestic cells with U.S. assembly, compared to imported cells. Anza says reasons for high demand are that manufacturers want to take advantage of incentives and mitigate tariff risk.

The Q2 report shows a slight price increase (4.3%) of cells from December to March, driven by tightening supply. However, Anza notes that the cost of modules that combine imported cells with U.S. assembled options has not risen as anticipated. Instead, prices have generally flattened and even declined by 0.4% from December 2024 to March 2025, potentially because buyers require higher domestic content points, which only modules with U.S. made cells can provide. Imported modules have experienced a 6.7% price decrease from December 2024 to 2025.

Anza cautions that current pricing data extends through March 2025 and doesn’t reflect the effects of new tariffs. Uncertainty around universal and reciprocal tariffs will likely drive up prices. The company also notes that trends highlighted in this report are based on current supplier commitments and are subject to change as policies and market dynamics evolve.