The three major electric utilities in California have actively pushed an agenda to inhibit the growth of rooftop solar, the one technology solution that represents an existential threat to their monopoly on electricity sales in the state, according to Bernadette Del Chiaro, executive director of the California Solar and Storage Association (CALSSA) during the pv magazine USA Week event in October.

A series of rulemaking decisions backed by the three utilities PG&E, SCE, and SDG&E have gained support from the California Public Utilities Commission (CPUC) which has moved in lockstep to gut rooftop solar.

In the past two years, the fight against rooftop solar in California has been an assault. California has gutted net metering, or the payment for exporting solar from the home to the grid, by about 80%. It has created stringent labor rules for commercial solar installations with AB2143. It determined that multi-meter properties like schools and farms cannot use their own solar energy production and must sell it to the grid at a low price and buy it back at a significantly higher price.

In 2024 the assault on rooftop continued, as CPUC approved $24 monthly fixed charges that are paid even if 100% the home’s energy is provided by solar. These fixed charges, which are already double the national average, are legally uncapped and are likely to continue to rise, according to Del Chiaro. There’s also an ongoing threat that existing solar customers may have their net metering rates altered.

The rooftop solar market in California has crashed following these changes. The chart below, shared by Del Chiaro, shows the number of interconnection applications submitted to utilities in a given month. An enormous spike of applications came in as customers rushed to secure older, more lucrative net metering rates, and the subsequent crash was the state of the market moving into NEM 3.0.

The chart debunks a few of the foundations of why NEM 3.0 was passed. It refutes that rooftop solar customers are only upper-class, while middle and low-income Californians are left behind, Del Chiaro said. It also refutes the suggestion that while solar installations may slow, more battery energy storage will be installed, stabilizing the grid. While it is true that batteries jumped from being included in 15% of projects to over 60%, the drop of installations led to a lower total volume of storage installations, she noted.

A year after the passage of NEM 3.0, major solar insurance provider Solar Insure said that 75% of California rooftop solar providers were at risk of bankruptcy. And since that time, several major installers have gone under.

Maintaining a monopoly

For Californians rooftop solar represents an opportunity to stem the tide of ever-increasing electricity prices, making it clear what power will cost for the next 20-25 years or more. But for utilities, it represents competition.

Utilities have sought to stamp out this competition by proliferating the idea that rooftop solar creates a “cost shift,” making the grid more expensive to operate and causing non-solar customers to pay higher bills. Del Chiaro described the “cost shift” not as an argument, but as a myth.

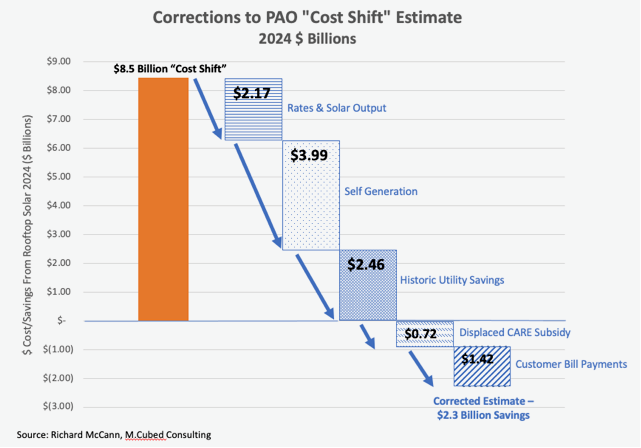

This August, the CPUC Public Advocates Office (PAO) which has sided with the investor-owned utilities requests on all of the above rulemaking decisions, issued a report outlining the impact of the cost shift. It assessed that rooftop solar will create $8.5 billion in extra costs for customers of the three investor-owned utilities. This has been the primary basis for the numerous anti-rooftop solar rulemaking decisions mentioned above.

However, this utility-forwarded cost shift argument has been debunked. Lawrence Berkeley Laboratory found that 47 states have a negligible solar power cost shift. Most states have solar penetration levels far below 10%. Until you hit that level of penetration there’s no cost shift altogether, yet states across the country are following California’s footsteps in slashing net metering.

Even at penetration levels of 10% or higher, the national laboratory found that the “shift” is only 5/1,000 of a cent per kilowatt-hour. Sixteen state-level analyses have come to the same conclusion that the cost shift is negligible.

“If the goal is to keep prices low, there are other pieces of the puzzle that affect rates far more than net metering,” Galen L. Barbose, a research scientist at LBNL, echoing a study by LBNL which put this in context. “Carbon pricing, operating outdated plants—those are the issues utilities and regulators should be focused on.”

Recent analysis by M.Cubed Consulting suggested that rooftop solar does not create net costs but represents a $2.3 billion net benefit on utility bills.

(Read: “Are California’s electricity prices rising because customers are installing solar panels?”)

Much of the rooftop solar cost shift analysis is based on the foundation that all grid costs are fixed and do not change over time. Therefore, as more people go solar, these fixed costs are paid by those who don’t have solar. However, over the last 20 years, despite flat electricity usage, transmission and distribution spending by utilities has increased 300%.

Far outpacing inflation, electricity rates have ballooned in California. CALSSA argues that the fundamental structure of private utilities in the state has created a perverse inventive to spend inefficiently. The more capital that utilities spend on infrastructure, the more they can get electricity rate increases approved. The more rates are increased, the larger the profits.

“Getting the utility to stop fighting customer solar is ultimately the thing that is needed in California and around the world,” said CALSSA Policy Director Brad Heavner. “We’ve had it in our head for years, how do we change this perverse incentive? It’s a hard thing to undertake but I’m hearing more talk about it.”

The California Air Resources Board projects that the state needs to add about 10 GW of solar per year to meet its goal of 100% emissions-free power by 2035. Over the past four years, the rooftop solar and storage market has accounted for 40% of capacity additions, which have yet to reach a 10 GW total in a single year. CALSSA argues that the state will need a strong mix of both rooftop solar and utility-scale solar to meet its goals. A healthy mix of project types from large-scale to rooftop gives Californians their best chance to secure control over the state’s ongoing electricity affordability crisis.

Watch a discussion of this topic from pv magazine USA Week in the video below, starting at hour 2:14.

Popular content